All Categories

Featured

Table of Contents

Insurance provider will not pay a small. Rather, think about leaving the cash to an estate or depend on. For more thorough info on life insurance policy get a duplicate of the NAIC Life Insurance Policy Buyers Guide.

The IRS places a limit on just how much cash can go into life insurance policy premiums for the plan and exactly how rapidly such premiums can be paid in order for the policy to preserve every one of its tax obligation advantages. If specific restrictions are surpassed, a MEC results. MEC insurance policy holders might undergo taxes on circulations on an income-first basis, that is, to the level there is gain in their policies, in addition to fines on any type of taxed quantity if they are not age 59 1/2 or older.

Please note that superior car loans build up rate of interest. Earnings tax-free treatment additionally thinks the loan will at some point be satisfied from income tax-free fatality advantage earnings. Loans and withdrawals decrease the plan's cash money worth and survivor benefit, may trigger certain policy benefits or cyclists to come to be inaccessible and might boost the chance the policy might lapse.

4 This is provided with a Lasting Care Servicessm rider, which is available for an added fee. In addition, there are limitations and constraints. A client might qualify for the life insurance policy, but not the rider. It is paid as an acceleration of the fatality benefit. A variable universal life insurance policy contract is an agreement with the key purpose of offering a death benefit.

What are the top Term Life providers in my area?

These profiles are closely managed in order to satisfy stated investment purposes. There are charges and costs connected with variable life insurance policy agreements, including death and threat fees, a front-end tons, administrative costs, investment administration costs, abandonment charges and charges for optional motorcyclists. Equitable Financial and its associates do not provide legal or tax obligation suggestions.

Whether you're beginning a family members or getting wedded, individuals normally begin to think of life insurance policy when somebody else begins to rely on their ability to make an income. And that's wonderful, because that's precisely what the survivor benefit is for. As you find out extra concerning life insurance, you're most likely to find that lots of plans for circumstances, entire life insurance policy have more than just a survivor benefit.

What are the advantages of whole life insurance policy? Here are a few of the crucial points you must recognize. One of the most attractive benefits of purchasing an entire life insurance plan is this: As long as you pay your premiums, your survivor benefit will never ever expire. It is guaranteed to be paid no matter when you die, whether that's tomorrow, in 5 years, 80 years and even better away. Premium plans.

Believe you do not require life insurance policy if you do not have youngsters? There are many benefits to having life insurance, even if you're not supporting a family.

Who are the cheapest Long Term Care providers?

Funeral costs, interment expenses and medical expenses can include up. Permanent life insurance is offered in different quantities, so you can choose a fatality benefit that meets your requirements.

Identify whether term or permanent life insurance policy is appropriate for you. Get a quote of exactly how much coverage you might need, and exactly how much it might cost. Find the correct amount for your budget plan and tranquility of mind. Discover your amount. As your individual situations modification (i.e., marriage, birth of a child or work promo), so will certainly your life insurance needs.

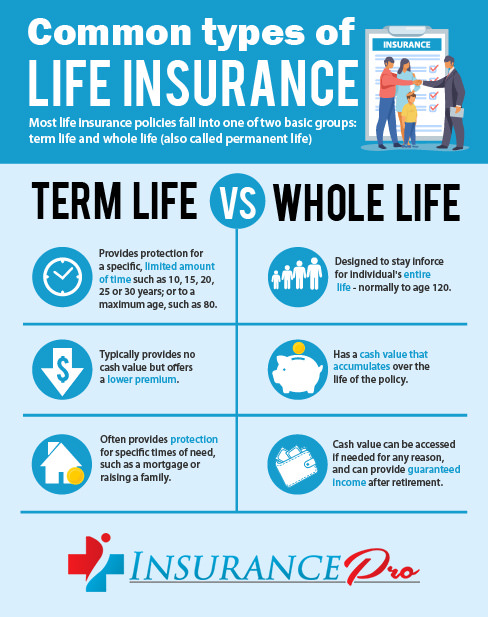

Generally, there are two kinds of life insurance prepares - either term or irreversible plans or some mix of both. Life insurance companies use different types of term plans and conventional life plans along with "rate of interest delicate" items which have come to be a lot more common because the 1980's.

Term insurance coverage gives defense for a specified period of time. This duration could be as short as one year or give coverage for a details number of years such as 5, 10, 20 years or to a specified age such as 80 or in many cases as much as the earliest age in the life insurance policy mortality.

What are the benefits of Income Protection?

Currently term insurance prices are extremely competitive and amongst the most affordable historically knowledgeable. It should be kept in mind that it is a widely held belief that term insurance coverage is the least expensive pure life insurance policy protection offered. One requires to assess the plan terms thoroughly to choose which term life options appropriate to satisfy your particular scenarios.

With each brand-new term the costs is boosted. The right to restore the policy without proof of insurability is a vital benefit to you. Or else, the risk you take is that your health and wellness may weaken and you may be incapable to acquire a policy at the very same prices or even in all, leaving you and your beneficiaries without protection.

The size of the conversion duration will vary depending on the type of term policy purchased. The costs price you pay on conversion is generally based on your "present obtained age", which is your age on the conversion date.

Under a level term policy the face amount of the policy stays the same for the entire period. Commonly such plans are marketed as home loan protection with the quantity of insurance coverage lowering as the balance of the home mortgage reduces.

What types of Senior Protection are available?

Traditionally, insurers have actually not deserved to transform costs after the policy is sold. Considering that such policies may proceed for years, insurance firms need to make use of traditional death, passion and expense rate estimates in the premium estimation. Adjustable costs insurance coverage, however, permits insurance providers to supply insurance policy at reduced "current" costs based upon less conservative assumptions with the right to alter these premiums in the future.

While term insurance coverage is developed to give protection for a defined period, irreversible insurance is developed to give coverage for your entire lifetime. To keep the costs price degree, the costs at the younger ages exceeds the real expense of defense. This added premium builds a book (money value) which aids pay for the policy in later years as the expense of defense rises over the premium.

Under some plans, costs are required to be spent for a set variety of years. Under other plans, costs are paid throughout the policyholder's life time. The insurance provider invests the excess premium dollars This kind of plan, which is occasionally called cash money worth life insurance policy, creates a financial savings component. Cash worths are essential to an irreversible life insurance policy plan.

{kind=link}

Latest Posts

Cheap Funeral Insurance

Final Expense Life Insurance Mortgage Protection Life Insurance

Family Funeral Insurance