All Categories

Featured

Table of Contents

Premiums are generally reduced than whole life policies. With a degree term plan, you can select your insurance coverage quantity and the policy length. You're not locked into an agreement for the remainder of your life. Throughout your plan, you never need to bother with the premium or survivor benefit amounts altering.

And you can't squander your plan during its term, so you won't obtain any kind of economic gain from your past coverage. As with various other sorts of life insurance, the expense of a level term plan relies on your age, insurance coverage demands, employment, way of living and health and wellness. Normally, you'll discover more cost effective coverage if you're more youthful, healthier and less dangerous to guarantee.

Since level term costs remain the very same for the period of insurance coverage, you'll recognize precisely how much you'll pay each time. That can be a huge assistance when budgeting your costs. Level term protection also has some adaptability, allowing you to tailor your policy with added attributes. These often been available in the kind of motorcyclists.

You may have to meet details conditions and certifications for your insurer to enact this cyclist. There additionally could be an age or time limit on the coverage.

Where can I find Level Term Life Insurance Calculator?

The fatality benefit is usually smaller, and coverage generally lasts up until your child turns 18 or 25. This biker might be an extra economical method to aid guarantee your children are covered as cyclists can often cover numerous dependents at the same time. As soon as your youngster ages out of this insurance coverage, it may be feasible to transform the motorcyclist into a brand-new policy.

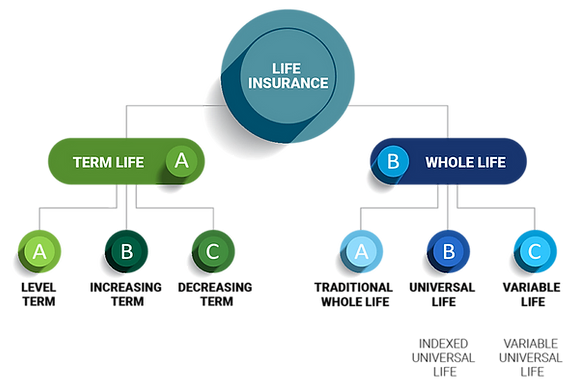

When contrasting term versus permanent life insurance policy, it's important to keep in mind there are a few various types. The most usual kind of long-term life insurance policy is whole life insurance policy, but it has some vital differences contrasted to level term coverage. Below's a standard review of what to think about when contrasting term vs.

Whole life insurance coverage lasts forever, while term coverage lasts for a specific duration. The premiums for term life insurance are typically less than whole life insurance coverage. With both, the costs continue to be the same for the period of the plan. Entire life insurance has a cash money worth component, where a portion of the premium might grow tax-deferred for future needs.

What Is Level Term Life Insurance?

One of the highlights of level term protection is that your premiums and your death benefit do not transform. With reducing term life insurance, your costs continue to be the exact same; nevertheless, the survivor benefit quantity gets smaller sized in time. You might have coverage that starts with a fatality benefit of $10,000, which could cover a mortgage, and after that each year, the fatality benefit will certainly decrease by a collection quantity or percentage.

Due to this, it's frequently a more economical kind of degree term protection., yet it may not be sufficient life insurance policy for your requirements.

After picking a policy, complete the application. For the underwriting procedure, you may have to give general individual, health, lifestyle and work info. Your insurance firm will certainly identify if you are insurable and the danger you may provide to them, which is shown in your premium prices. If you're authorized, sign the paperwork and pay your first premium.

Lastly, think about scheduling time annually to assess your plan. You might intend to upgrade your beneficiary info if you've had any kind of substantial life changes, such as a marriage, birth or divorce. Life insurance policy can sometimes feel difficult. You do not have to go it alone. As you explore your choices, take into consideration reviewing your needs, desires and interests in an economic professional.

Level Term Life Insurance Companies

No, degree term life insurance does not have cash worth. Some life insurance policy policies have an investment function that enables you to develop cash money worth in time. Level term life insurance for families. A part of your costs payments is reserved and can gain passion over time, which grows tax-deferred during the life of your coverage

These policies are commonly considerably extra costly than term coverage. If you get to the end of your policy and are still to life, the protection finishes. Nevertheless, you have some alternatives if you still desire some life insurance protection. You can: If you're 65 and your coverage has actually run out, for instance, you might wish to purchase a new 10-year level term life insurance plan.

What are the benefits of Level Term Life Insurance Protection?

You might be able to transform your term coverage into a whole life policy that will certainly last for the rest of your life. Lots of kinds of degree term plans are convertible. That indicates, at the end of your coverage, you can transform some or every one of your plan to whole life coverage.

Degree term life insurance coverage is a plan that lasts a collection term typically in between 10 and thirty years and comes with a degree fatality advantage and degree premiums that stay the exact same for the entire time the policy holds. This implies you'll understand precisely just how much your settlements are and when you'll have to make them, allowing you to budget plan as necessary.

Degree term can be a fantastic option if you're aiming to acquire life insurance protection for the very first time. According to LIMRA's 2023 Insurance policy Barometer Research Study, 30% of all grownups in the U.S (Level term life insurance for families). requirement life insurance coverage and do not have any type of type of policy. Degree term life is foreseeable and budget friendly, which makes it among the most popular sorts of life insurance policy

A 30-year-old male with a comparable profile can expect to pay $29 monthly for the exact same protection. AgeGender$250,000 coverage amount$500,000 insurance coverage amount$1 million insurance coverage amount20Female$15$23$34Male$19$29$4830Female$15$23$37Male$18$29$4940Female$22$35$61Male$25$43$7550Female$44$78$139Male$57$102$18860Female$108$194$355Male$149$268$500 Collapse table Method: Ordinary regular monthly prices are computed for male and women non-smokers in a Preferred health and wellness category getting a 20-year $250,000, $500,000, or $1,000,000 term life insurance policy plan.

Why is Level Term Life Insurance Policy important?

Prices may vary by insurer, term, protection quantity, wellness course, and state. Not all policies are offered in all states. Rate illustration legitimate as of 09/01/2024. It's the most inexpensive type of life insurance policy for most individuals. Degree term life is a lot more inexpensive than an equivalent whole life insurance plan. It's very easy to manage.

It enables you to spending plan and strategy for the future. You can conveniently factor your life insurance right into your budget because the costs never ever change. You can plan for the future equally as conveniently due to the fact that you recognize precisely just how much cash your loved ones will receive in the event of your lack.

What is the most popular Level Term Life Insurance Premiums plan in 2024?

This holds true for people that quit smoking or that have a health problem that fixes. In these instances, you'll normally need to go with a brand-new application procedure to obtain a far better price. If you still require protection by the time your degree term life plan nears the expiry day, you have a few options.

{kind=link}

Latest Posts

Cheap Funeral Insurance

Final Expense Life Insurance Mortgage Protection Life Insurance

Family Funeral Insurance